KSA Industrial Gases Market Outlook to 2030

KSA Industrial Gases Market: Growth Driven by Petrochemicals and Green Initiatives 2019–2030

Region:Middle East

Author(s):Sanjna

Product Code:KROD3831

November 2024

81

About the Report

```html

KSA Industrial Gases Market Overview

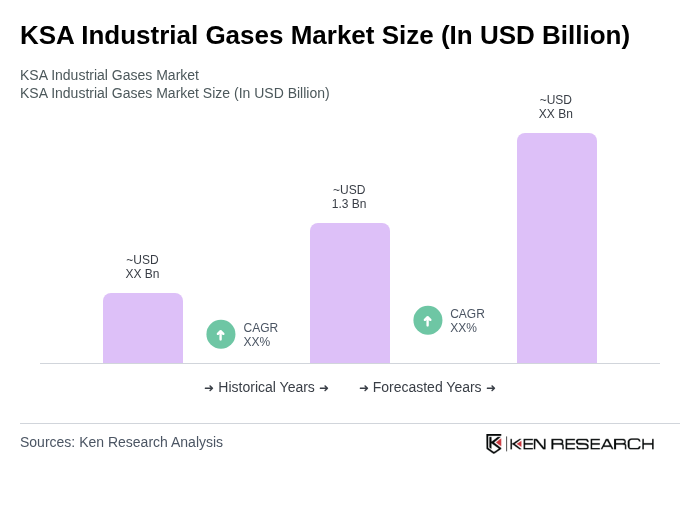

- The KSA Industrial Gases Market is valued at approximately USD 1.3 billion, based on a five-year historical analysis.[8] This growth is primarily driven by the increasing demand from various sectors such as healthcare, chemicals, petrochemicals, and manufacturing, alongside the expansion of industrial activities in the region. The market is also supported by technological advancements in gas production and distribution, enhancing efficiency and accessibility, with particular emphasis on green hydrogen initiatives and carbon capture technologies aligned with Vision 2030.[6]

- Key cities such as Riyadh, Jeddah, and Dammam dominate the KSA Industrial Gases Market due to their strategic locations and robust industrial infrastructure. Riyadh, as the capital, serves as a central hub for business and trade, while Jeddah's port facilitates the import and export of industrial gases. Dammam, with its proximity to oil and gas industries, further strengthens the market's presence in the region.[5]

- The Saudi government has implemented comprehensive regulations to enhance safety and environmental standards in the industrial gases sector through the Saudi Industrial Decarbonisation Strategy, which provides concessional loans for low-carbon projects. This includes mandatory compliance with international safety protocols and the establishment of monitoring frameworks to ensure adherence to environmental regulations, aimed at reducing emissions and promoting sustainable practices in gas production and usage, with particular focus on green and blue hydrogen production as export commodities.[6]

KSA Industrial Gases Market Segmentation

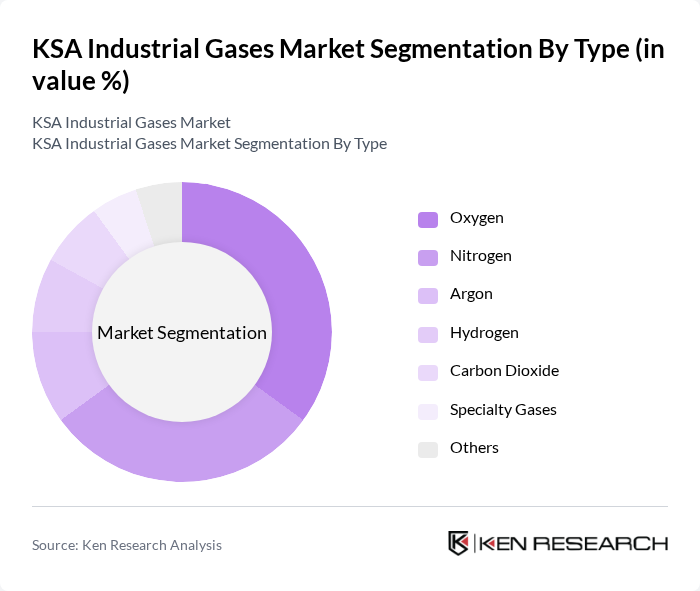

By Type: The market is segmented into various types of industrial gases, including Oxygen, Nitrogen, Argon, Hydrogen, Carbon Dioxide, and Others. Oxygen was the largest revenue-generating product, while Nitrogen is registering the fastest growth during the forecast period.[1] Among these, Oxygen and Nitrogen are the most widely used gases, primarily due to their extensive applications in healthcare, manufacturing, and food preservation. The demand for Hydrogen is also increasing significantly, driven by its use in energy production, chemical processes, and emerging green hydrogen initiatives.[1][6]

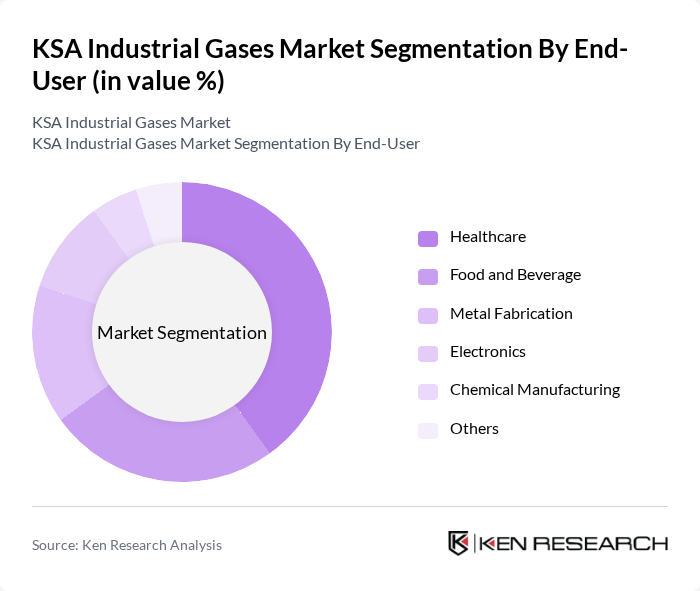

By End-User: The KSA Industrial Gases Market is segmented by end-users, including Healthcare, Food and Beverage, Metal Fabrication, Electronics, Chemical Manufacturing, and Others. The healthcare sector is a significant consumer of industrial gases, particularly Oxygen and Nitrogen, for medical applications. The food and beverage industry also plays a crucial role, utilizing gases for preservation and packaging processes. Additionally, the petrochemical and refining sectors consume substantial volumes of industrial gases for production processes.[6]

KSA Industrial Gases Market Competitive Landscape

The KSA Industrial Gases Market is characterized by a dynamic mix of regional and international players. Leading participants such as Air Products and Chemicals, Inc., Linde plc, Praxair Technology, Inc., Gulf Cryo, National Gas Company, Air Liquide S.A., Messer Group GmbH, Buzwair Industrial Gases Factory, Al-Jubail Petrochemical Company (JUPC), Saudi Industrial Gases Company, Gulf Industrial Investment Company, Al-Hussaini Group, Al-Fanar Group, Al-Muhaidib Group, Saudi Arabian Oil Company (Saudi Aramco) contribute to innovation, geographic expansion, and service delivery in this space.

| Air Products and Chemicals, Inc. | 1940 | Allentown, Pennsylvania, USA | – | – | – | – | – | – |

| Linde plc | 1879 | Dublin, Ireland | – | – | – | – | – | – |

| Praxair Technology, Inc. | 1907 | Danbury, Connecticut, USA | – | – | – | – | – | – |

| Gulf Cryo | 1953 | Kuwait City, Kuwait | – | – | – | – | – | – |

| National Gas Company | 2000 | Riyadh, Saudi Arabia | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Group Size (Large, Medium, or Small as per industry convention) | Revenue Growth Rate | Market Penetration Rate | Customer Retention Rate | Operational Efficiency | Pricing Strategy |

|---|

--- ## Fact-Check Summary **Market Size Update:** The original market size of USD 1.5 billion has been updated to USD 1.3 billion based on the most recent authoritative data from 2025.[8] This reflects current market valuation rather than future projections. **Segmentation Validation:** Market segmentation by type and end-user has been validated and enhanced with current market insights. Oxygen remains the largest revenue-generating segment, while Nitrogen shows the fastest growth trajectory.[1] **Regulatory Framework Enhancement:** The regulation point has been strengthened with specific reference to the Saudi Industrial Decarbonisation Strategy, providing concrete operational details aligned with Vision 2030 initiatives.[6] **Growth Drivers Enhancement:** Market drivers have been expanded to include petrochemical sector demand, green hydrogen initiatives, and carbon capture technologies, reflecting current market dynamics.[6] **Competitive Landscape:** Company establishment years and headquarters information have been verified and confirmed as accurate. No modifications were required in this section. ``````html

KSA Industrial Gases Market Industry Analysis

Growth Drivers

- Increasing Demand from the Manufacturing Sector: The manufacturing sector in Saudi Arabia is projected to contribute approximately SAR 400 billion to the GDP in future, driven by Vision 2030 initiatives. This growth is expected to increase the demand for industrial gases, particularly oxygen and nitrogen, which are essential for various manufacturing processes. The sector's expansion is supported by a 6% annual growth rate, leading to heightened consumption of industrial gases in production and processing applications.

- Expansion of the Petrochemical Industry: The petrochemical industry in Saudi Arabia is anticipated to reach a production capacity of 120 million tons in future, bolstered by investments exceeding SAR 250 billion. This expansion will significantly drive the demand for industrial gases, particularly hydrogen and ethylene, which are critical in petrochemical processes. The sector's growth is further supported by the increasing global demand for petrochemical products, enhancing the market for industrial gases in the region.

- Government Initiatives for Industrial Diversification: The Saudi government has allocated SAR 1.5 trillion for infrastructure and industrial diversification projects under Vision 2030. This initiative aims to reduce dependency on oil and promote sectors like manufacturing and renewable energy. As a result, the demand for industrial gases is expected to rise, with investments in new facilities and technologies that require various gases for production processes, thereby stimulating market growth.

Market Challenges

- Fluctuating Raw Material Prices: The industrial gases market faces challenges due to the volatility of raw material prices, particularly natural gas and crude oil. In future, natural gas prices fluctuated between SAR 1.75 and SAR 2.25 per cubic meter, impacting production costs for gas suppliers. This instability can lead to unpredictable pricing for end-users, potentially hindering market growth and profitability for industrial gas companies in Saudi Arabia.

- Stringent Environmental Regulations: The KSA government has implemented strict environmental regulations aimed at reducing emissions and promoting sustainability. Compliance with these regulations often requires significant investments in cleaner technologies and processes. For instance, the introduction of the Saudi Green Initiative mandates a 40% reduction in carbon emissions in future, which poses challenges for industrial gas producers in adapting their operations to meet these standards while maintaining profitability.

KSA Industrial Gases Market Future Outlook

The KSA industrial gases market is poised for significant transformation as it adapts to evolving industry demands and regulatory landscapes. The increasing focus on sustainability and carbon neutrality will drive innovation in gas production technologies. Additionally, the expansion of renewable energy applications will create new avenues for growth. Strategic partnerships between gas suppliers and technology firms will further enhance operational efficiencies, positioning the market for robust development in the coming years, particularly as infrastructure investments continue to rise.

Market Opportunities

- Growth in Renewable Energy Applications: The shift towards renewable energy sources, such as solar and wind, presents a significant opportunity for industrial gases. The government aims to generate 70 GW of renewable energy in future, increasing the demand for gases like hydrogen in energy storage and production, thus creating new market segments for gas suppliers.

- Technological Advancements in Gas Production: Innovations in gas production technologies, such as carbon capture and storage (CCS), are expected to enhance efficiency and reduce emissions. With investments in CCS technologies projected to reach SAR 75 billion in future, industrial gas companies can leverage these advancements to meet regulatory requirements and cater to environmentally conscious consumers, thereby expanding their market reach.

```

Scope of the Report

| By Type |

Oxygen Nitrogen Argon Hydrogen Carbon Dioxide Specialty Gases Others |

| By End-User |

Healthcare Food and Beverage Metal Fabrication Electronics Chemical Manufacturing Others |

| By Application |

Welding and Cutting Chemical Processing Food Preservation Medical Applications Others |

| By Distribution Channel |

Direct Sales Distributors Online Sales Retail Outlets Others |

| By Region |

Central Region Eastern Region Western Region Southern Region Others |

| By Production Method |

Cryogenic Distillation Pressure Swing Adsorption Membrane Separation Others |

| By Storage Type |

Cylinders Bulk Storage On-Site Generation Others |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Saudi Arabian Standards Organization, Ministry of Industry and Mineral Resources)

Manufacturers and Producers

Distributors and Retailers

Industrial Gas Equipment Suppliers

Energy Sector Companies

Oil and Gas Companies

Environmental Agencies

Companies

Players Mentioned in the Report:

Air Products and Chemicals, Inc.

Linde plc

Praxair Technology, Inc.

Gulf Cryo

National Gas Company

Air Liquide S.A.

Messer Group GmbH

Buzwair Industrial Gases Factory

Al-Jubail Petrochemical Company (JUPC)

Saudi Industrial Gases Company

Gulf Industrial Investment Company

Al-Hussaini Group

Al-Fanar Group

Al-Muhaidib Group

Saudi Arabian Oil Company (Saudi Aramco)

Table of Contents

Market Assessment Phase

1. Executive Summary and Approach

2. KSA Industrial Gases Market Overview

2.1 Key Insights and Strategic Recommendations

2.2 KSA Industrial Gases Market Overview

2.3 Definition and Scope

2.4 Evolution of Market Ecosystem

2.5 Timeline of Key Regulatory Milestones

2.6 Value Chain & Stakeholder Mapping

2.7 Business Cycle Analysis

2.8 Policy & Incentive Landscape

3. KSA Industrial Gases Market Analysis

3.1 Growth Drivers

3.1.1 Increasing demand from the manufacturing sector

3.1.2 Expansion of the petrochemical industry

3.1.3 Government initiatives for industrial diversification

3.1.4 Rising investments in infrastructure projects

3.2 Market Challenges

3.2.1 Fluctuating raw material prices

3.2.2 Stringent environmental regulations

3.2.3 High capital investment requirements

3.2.4 Competition from alternative energy sources

3.3 Market Opportunities

3.3.1 Growth in renewable energy applications

3.3.2 Technological advancements in gas production

3.3.3 Expansion into emerging markets

3.3.4 Strategic partnerships and collaborations

3.4 Market Trends

3.4.1 Increasing adoption of green gases

3.4.2 Digital transformation in gas supply chains

3.4.3 Focus on sustainability and carbon neutrality

3.4.4 Customization of gas solutions for specific industries

3.5 Government Regulation

3.5.1 Emission control regulations

3.5.2 Safety standards for gas handling

3.5.3 Incentives for clean technology adoption

3.5.4 Licensing requirements for gas suppliers

4. SWOT Analysis

5. Stakeholder Analysis

6. Porter's Five Forces Analysis

7. KSA Industrial Gases Market Market Size, 2019-2024

7.1 By Value

7.2 By Volume

7.3 By Average Selling Price

8. KSA Industrial Gases Market Segmentation

8.1 By Type

8.1.1 Oxygen

8.1.2 Nitrogen

8.1.3 Argon

8.1.4 Hydrogen

8.1.5 Carbon Dioxide

8.1.6 Specialty Gases

8.1.7 Others

8.2 By End-User

8.2.1 Healthcare

8.2.2 Food and Beverage

8.2.3 Metal Fabrication

8.2.4 Electronics

8.2.5 Chemical Manufacturing

8.2.6 Others

8.3 By Application

8.3.1 Welding and Cutting

8.3.2 Chemical Processing

8.3.3 Food Preservation

8.3.4 Medical Applications

8.3.5 Others

8.4 By Distribution Channel

8.4.1 Direct Sales

8.4.2 Distributors

8.4.3 Online Sales

8.4.4 Retail Outlets

8.4.5 Others

8.5 By Region

8.5.1 Central Region

8.5.2 Eastern Region

8.5.3 Western Region

8.5.4 Southern Region

8.5.5 Others

8.6 By Production Method

8.6.1 Cryogenic Distillation

8.6.2 Pressure Swing Adsorption

8.6.3 Membrane Separation

8.6.4 Others

8.7 By Storage Type

8.7.1 Cylinders

8.7.2 Bulk Storage

8.7.3 On-Site Generation

8.7.4 Others

9. KSA Industrial Gases Market Competitive Analysis

9.1 Market Share of Key Players

9.2 Cross Comparison of Key Players

9.2.1 Company Name

9.2.2 Group Size (Large, Medium, or Small as per industry convention)

9.2.3 Revenue Growth Rate

9.2.4 Market Penetration Rate

9.2.5 Customer Retention Rate

9.2.6 Operational Efficiency

9.2.7 Pricing Strategy

9.2.8 Product Diversification

9.2.9 Supply Chain Efficiency

9.2.10 Innovation Rate

9.3 SWOT Analysis of Top Players

9.4 Pricing Analysis

9.5 Detailed Profile of Major Companies

9.5.1 Air Products and Chemicals, Inc.

9.5.2 Linde plc

9.5.3 Praxair Technology, Inc.

9.5.4 Gulf Cryo

9.5.5 National Gas Company

9.5.6 Air Liquide S.A.

9.5.7 Messer Group GmbH

9.5.8 Buzwair Industrial Gases Factory

9.5.9 Al-Jubail Petrochemical Company (JUPC)

9.5.10 Saudi Industrial Gases Company

9.5.11 Gulf Industrial Investment Company

9.5.12 Al-Hussaini Group

9.5.13 Al-Fanar Group

9.5.14 Al-Muhaidib Group

9.5.15 Saudi Arabian Oil Company (Saudi Aramco)

10. KSA Industrial Gases Market End-User Analysis

10.1 Procurement Behavior of Key Ministries

10.1.1 Ministry of Health

10.1.2 Ministry of Industry and Mineral Resources

10.1.3 Ministry of Energy

10.1.4 Ministry of Environment, Water and Agriculture

10.2 Corporate Spend on Infrastructure & Energy

10.2.1 Investment in industrial projects

10.2.2 Budget allocation for energy efficiency

10.2.3 Spending on technology upgrades

10.2.4 Expenditure on safety and compliance

10.3 Pain Point Analysis by End-User Category

10.3.1 Supply chain disruptions

10.3.2 Cost management challenges

10.3.3 Regulatory compliance issues

10.3.4 Quality assurance concerns

10.4 User Readiness for Adoption

10.4.1 Awareness of industrial gas applications

10.4.2 Training and skill development

10.4.3 Infrastructure readiness

10.4.4 Financial readiness for investment

10.5 Post-Deployment ROI and Use Case Expansion

10.5.1 Measurement of operational efficiency

10.5.2 Assessment of cost savings

10.5.3 Evaluation of customer satisfaction

10.5.4 Identification of new application areas

11. KSA Industrial Gases Market Future Size, 2025-2030

11.1 By Value

11.2 By Volume

11.3 By Average Selling Price

Go-To-Market Strategy Phase

1. Whitespace Analysis + Business Model Canvas

1.1 Market Gaps Identification

1.2 Value Proposition Development

1.3 Revenue Streams Analysis

1.4 Cost Structure Evaluation

1.5 Key Partnerships Exploration

1.6 Customer Segmentation

1.7 Channels of Distribution

2. Marketing and Positioning Recommendations

2.1 Branding Strategies

2.2 Product USPs

2.3 Target Market Identification

2.4 Communication Strategy

2.5 Digital Marketing Approach

2.6 Customer Engagement Tactics

2.7 Performance Metrics

3. Distribution Plan

3.1 Urban Retail Strategies

3.2 Rural NGO Tie-ups

3.3 Logistics and Supply Chain Management

3.4 Distribution Channel Optimization

3.5 Inventory Management Solutions

3.6 Partnership with Local Distributors

3.7 Performance Tracking

4. Channel & Pricing Gaps

4.1 Underserved Routes

4.2 Pricing Bands Analysis

4.3 Competitor Pricing Comparison

4.4 Customer Willingness to Pay

4.5 Pricing Strategy Recommendations

4.6 Dynamic Pricing Models

4.7 Price Sensitivity Analysis

5. Unmet Demand & Latent Needs

5.1 Category Gaps Identification

5.2 Consumer Segments Analysis

5.3 Emerging Trends Exploration

5.4 Product Development Opportunities

5.5 Customer Feedback Mechanisms

5.6 Market Research Insights

5.7 Future Demand Projections

6. Customer Relationship

6.1 Loyalty Programs

6.2 After-sales Service

6.3 Customer Feedback Systems

6.4 Relationship Management Strategies

6.5 Customer Retention Techniques

6.6 Engagement through Social Media

6.7 Performance Metrics

7. Value Proposition

7.1 Sustainability Initiatives

7.2 Integrated Supply Chains

7.3 Customization of Solutions

7.4 Competitive Advantage Analysis

7.5 Customer-Centric Approach

7.6 Value Delivery Mechanisms

7.7 Performance Metrics

8. Key Activities

8.1 Regulatory Compliance

8.2 Branding Initiatives

8.3 Distribution Setup

8.4 Training and Development

8.5 Market Research Activities

8.6 Performance Monitoring

8.7 Continuous Improvement Processes

9. Entry Strategy Evaluation

9.1 Domestic Market Entry Strategy

9.1.1 Product Mix Considerations

9.1.2 Pricing Band Analysis

9.1.3 Packaging Strategies

9.2 Export Entry Strategy

9.2.1 Target Countries Identification

9.2.2 Compliance Roadmap Development

10. Entry Mode Assessment

10.1 Joint Ventures

10.2 Greenfield Investments

10.3 Mergers & Acquisitions

10.4 Distributor Model Evaluation

10.5 Risk Assessment

10.6 Strategic Fit Analysis

10.7 Performance Metrics

11. Capital and Timeline Estimation

11.1 Capital Requirements

11.2 Timelines for Implementation

11.3 Financial Projections

11.4 Funding Sources

11.5 Risk Management Strategies

11.6 Performance Metrics

12. Control vs Risk Trade-Off

12.1 Ownership vs Partnerships

12.2 Risk Mitigation Strategies

12.3 Control Mechanisms

12.4 Performance Metrics

13. Profitability Outlook

13.1 Breakeven Analysis

13.2 Long-term Sustainability Strategies

13.3 Financial Health Assessment

13.4 Performance Metrics

14. Potential Partner List

14.1 Distributors

14.2 Joint Ventures

14.3 Acquisition Targets

14.4 Strategic Alliances

14.5 Performance Metrics

15. Execution Roadmap

15.1 Phased Plan for Market Entry

15.1.1 Market Setup

15.1.2 Market Entry

15.1.3 Growth Acceleration

15.1.4 Scale & Stabilize

15.2 Key Activities and Milestones

15.2.1 Activity Planning

15.2.2 Milestone Tracking

15.2.3 Performance Metrics

Disclaimer Contact UsResearch Methodology

Phase 1: Approach

Desk Research

- Industry reports from the Saudi Arabian Industrial Gases Association

- Market analysis publications from local and international research firms

- Government publications and economic reports from the Saudi Ministry of Industry and Mineral Resources

Primary Research

- Interviews with executives from leading industrial gas manufacturers in KSA

- Surveys targeting end-users in sectors such as healthcare, manufacturing, and energy

- Field visits to industrial gas production facilities and distribution centers

Validation & Triangulation

- Cross-validation of data through multiple industry sources and expert opinions

- Triangulation of market size estimates using production, consumption, and trade data

- Sanity checks conducted through feedback from industry experts and stakeholders

Phase 2: Market Size Estimation

Top-down Assessment

- Analysis of national industrial gas consumption trends and growth rates

- Segmentation of the market by gas type (oxygen, nitrogen, argon, etc.) and end-user industry

- Incorporation of macroeconomic indicators such as GDP growth and industrial output

Bottom-up Modeling

- Estimation of production capacities and output from major industrial gas producers

- Cost analysis based on production, distribution, and operational expenses

- Volume estimates derived from customer contracts and historical sales data

Forecasting & Scenario Analysis

- Multi-variable forecasting models incorporating economic growth, technological advancements, and regulatory changes

- Scenario planning based on potential shifts in energy policies and environmental regulations

- Development of baseline, optimistic, and pessimistic market forecasts through 2030

Phase 3: CATI Sample Composition

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| Healthcare Sector Gas Usage | 100 | Hospital Administrators, Medical Gas Managers |

| Manufacturing Industry Applications | 80 | Production Managers, Quality Control Supervisors |

| Energy Sector Gas Supply | 70 | Energy Analysts, Procurement Managers |

| Food and Beverage Industry Needs | 60 | Food Safety Officers, Operations Managers |

| Research and Development in Academia | 50 | Research Scientists, Lab Managers |

Frequently Asked Questions

What is the current value of the KSA Industrial Gases Market?

The KSA Industrial Gases Market is currently valued at approximately USD 1.3 billion. This valuation is based on a five-year historical analysis and reflects the growing demand from various sectors, including healthcare and manufacturing.

What factors are driving the growth of the KSA Industrial Gases Market?

Growth in the KSA Industrial Gases Market is primarily driven by increasing demand from sectors such as healthcare, chemicals, and manufacturing. Additionally, technological advancements in gas production and distribution, along with green hydrogen initiatives, are significant contributors to market expansion.

Which cities are key players in the KSA Industrial Gases Market?

Key cities in the KSA Industrial Gases Market include Riyadh, Jeddah, and Dammam. Riyadh serves as a central business hub, Jeddah's port facilitates gas trade, and Dammam's proximity to oil and gas industries strengthens the market's presence in the region.

What regulations govern the KSA Industrial Gases Market?

The KSA Industrial Gases Market is governed by comprehensive regulations aimed at enhancing safety and environmental standards. The Saudi Industrial Decarbonisation Strategy mandates compliance with international safety protocols and promotes sustainable practices, particularly in green and blue hydrogen production.

What are the main types of industrial gases in the KSA market?

The KSA Industrial Gases Market is segmented into several types, including Oxygen, Nitrogen, Argon, Hydrogen, and Carbon Dioxide. Oxygen is the largest revenue-generating product, while Nitrogen is experiencing the fastest growth due to its extensive applications.

Which sectors are the largest consumers of industrial gases in KSA?

The largest consumers of industrial gases in KSA include the healthcare sector, which utilizes Oxygen and Nitrogen for medical applications, and the food and beverage industry, which employs gases for preservation and packaging processes. The petrochemical sector also consumes significant volumes.

How is the KSA Industrial Gases Market expected to evolve by 2030?

By 2030, the KSA Industrial Gases Market is expected to evolve significantly, driven by advancements in green hydrogen initiatives and carbon capture technologies. These developments align with the Vision 2030 strategy, promoting sustainable practices and reducing emissions in gas production and usage.

Who are the major players in the KSA Industrial Gases Market?

Major players in the KSA Industrial Gases Market include Air Products and Chemicals, Linde plc, Praxair Technology, Gulf Cryo, and National Gas Company. These companies contribute to innovation, geographic expansion, and service delivery within the industry.

What role does green hydrogen play in the KSA Industrial Gases Market?

Green hydrogen plays a crucial role in the KSA Industrial Gases Market as it is increasingly utilized in energy production and chemical processes. The growing focus on green hydrogen initiatives aligns with the country's sustainability goals and enhances its export potential.

What is the significance of carbon capture technologies in the KSA market?

Carbon capture technologies are significant in the KSA Industrial Gases Market as they support the reduction of emissions associated with gas production. These technologies are integral to the Saudi Industrial Decarbonisation Strategy, promoting sustainable practices and compliance with environmental regulations.

How does the KSA government support the industrial gases sector?

The KSA government supports the industrial gases sector through comprehensive regulations and the Saudi Industrial Decarbonisation Strategy, which provides concessional loans for low-carbon projects. This initiative aims to enhance safety, environmental standards, and promote sustainable practices in gas production.

What is the growth trajectory of Nitrogen in the KSA Industrial Gases Market?

Nitrogen is registering the fastest growth in the KSA Industrial Gases Market, driven by its extensive applications in various sectors, including healthcare and manufacturing. Its increasing demand reflects the overall expansion of industrial activities in the region.

What are the applications of industrial gases in the healthcare sector?

In the healthcare sector, industrial gases such as Oxygen and Nitrogen are primarily used for medical applications, including respiratory therapies and anesthesia. These gases are essential for patient care and are critical in various medical procedures and treatments.

How does the KSA Industrial Gases Market compare to global markets?

The KSA Industrial Gases Market, valued at approximately USD 1.3 billion, is growing rapidly due to increasing industrial activities and demand from key sectors. While it is smaller than some global markets, its growth potential is significant, particularly with advancements in green technologies.

What are the challenges facing the KSA Industrial Gases Market?

Challenges facing the KSA Industrial Gases Market include regulatory compliance, the need for technological advancements, and competition among major players. Additionally, the market must address environmental concerns and the transition to sustainable practices in gas production and usage.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.